How are your going to pay for all that time off?

According to a Metlife Mature Market Institute (MMI) look at the oldest of the baby boom generation those who will turn 62 in 2008 (and are eligible for those early Social Security payments) the average net worth of these soon-to-be retirees is $257,800 (excluding their home) and their average annual income is approximately $71,400.

According to MMI, 47 percent of these pre-retirees are covered by a defined benefit plan from their employer, 50 percent have a 401K, 50 percent have an IRA, 38 percent have stocks and an equal amount are invested in mutual funds.

Oh, and 31 percent of those 62-year-olds plan to take that first SSA payment this year.

But, do they have enough set aside to maintain their standard of living and cover the inevitable increase in all things, especially health care expenses for the next 20 or 30 years?

For that matter, do you?

As Allyn Freeman, co author of "Reworking Retirement" said, "longevity is one of the four horsemen of the apocalypse of retirement.

People are pushing way past their 80s into their 90s, and every year you live you need more income," he said.

What's your plan?

"The question you need to answer [is] 'what's it going to cost you on a month-by-month basis after you retire?'" David Rye, author of "The 250 Retirement Questions Everyone Should Ask" told PRIME.

He said this cost-analysis needs to consider not only the expected budgetary norms food, heat, insurance, prescriptions, taxes and such, but the other things you may want to do, such as travel, play golf, go back to school, relocate for half the year, etc.

"It's one thing to retire and say, 'I'm going to do all these things,' but [the question] is what's it going to take to do these things and live?" he said.

Rye said he hopes his book, and the information he gave PRIME, makes soon-to-be retirees (and those thinking about retirement in the next 10, 15 or even 20 years) aware that "they financially may not be ready to retire unless they are ready to make some adjustments to their standard of living once they retire."

This calculation is especially important given how poorly many people, particularly young boomers those now in their 50s have actually prepared for retirement expenses.

A report prepared by the education arm of Mass Mutual Life Insurance Company highlights this fact, stating "the personal savings rates of workers have been declining since the early 1990s. At the same time, rising premiums for Medicare, increased longevity and declining social Security replacement rates underscore the need for savings."

Rye's answer to this oxymoron of wants and assets is simple planning. Everyone, he said, no matter what stage of retirement they are at needs a solid retirement financial plan.

"They need to write it down," Rye said. "They need to study the numbers, and they need to decide if that is the right number [for what they want]."

"Somewhere in the overall scheme of things people must realize that [in retiring,] they are giving up a source of income that they have relied on all their lives," he said .

Working your plan

Rye said a solid retirement plan isn't something that you create once and forget about.

"Put something down and work on it on an ongoing basis," he said. "It's something that's going to change with time, as you would expect it to."

That plan should include all the sources of income a potential retiree expects to receive Social Security, any company pensions, and income from investments such as stocks, bonds IRAs and 401Ks.

"You've got a 401K plan; what is it invested in? Is it secure? Is it making any interest? Are there any alternatives?" he said.

Basically, he posed the question "have you looked at it lately?"

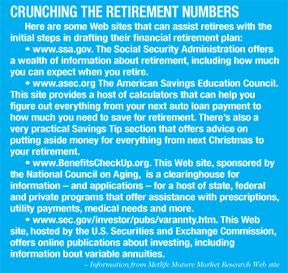

In his book, Rye said he included an appendix with Web sites that offer readers extensive information about the different methods of investing, as well as several sites, such as www.schwab.com, that offer free retirement planning tools.

"The Web, as you know, is an incredible resource for easy access to information," he said.

Once you have a working plan, Rye said to "have someone else look at it, a good friend who knows numbers better than you, maybe an accountant or a financial planner," he said.

What about early retirees?

In "Reworking Retirement," Freeman said this attention to income resources is even more important to individuals who are planning or hoping to retire before they reach their 60s.

"People 50, 55, 60 don't collect Social Security, so they can't plan that in when planning their [initial retirement] income," he said.

He also said these early retirees need to consider how they will handle big expenses, such as health care, before they qualify for government-sponsored programs such as Medicare.

"If I retire at 58, and I want to keep up my medical insurance; payments are very expensive. How will I pay for it?" he said. "Many people keep working to reach 65 to qualify for the less expensive Medicare."

No matter what age an individual targets for retirement, it's "all about the numbers," Rye said. "I keep coming back to the numbers because it's pretty well established that the biggest concern is money will they have enough money to retire?"

Part II of PRIME's Retirement Guide with a look at housing, insurance, estate and post-retirement work options will appear in the April issue.